Asset Allocation: The One Decision That Matters Most

Picking the right stocks matters less than you think. Your split between stocks, bonds, and cash determines 90% of your portfolio's long-term performance. Larry explains asset allocation without the jargon.

Larry "Big Short" Burry BEARISH

Senior Doomer Analyst

"Former death metal drummer turned market doomsayer. Predicts crashes using tea leaves and charts. His glass eye sees the future, and it's always red."

Here’s the statistic that will change how you think about investing: academic research shows that approximately 90% of a portfolio’s variability in returns over time is explained by its asset allocation — not by which individual stocks or funds you pick.

In other words, the big decision isn’t Apple vs. Google. It’s: how much in stocks, how much in bonds, how much in cash.

That’s asset allocation. And it’s the most important decision you’ll make as an investor.

What Are the Main Asset Classes?

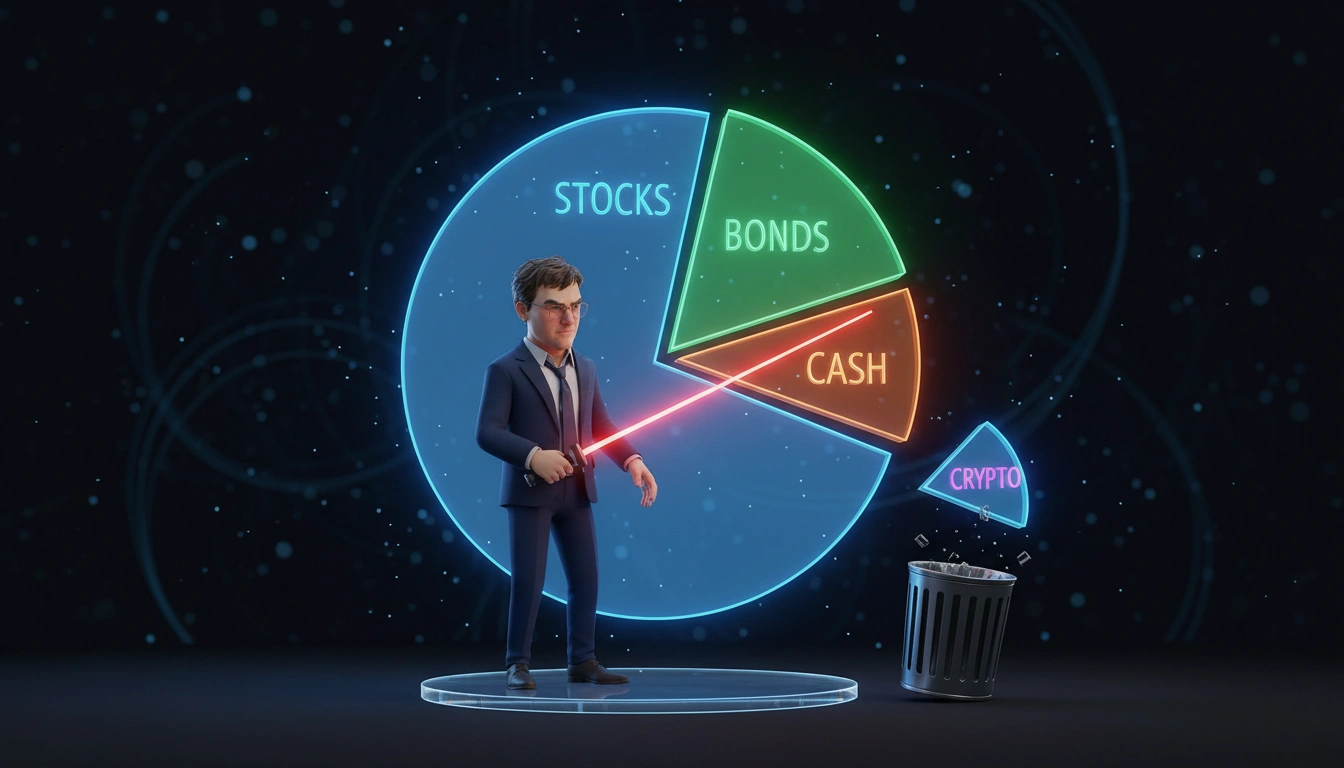

Stocks (Equities) Ownership stakes in companies. Historically highest long-term returns (~10% nominal, ~7.7% real). Also highest short-term volatility. S&P 500 has dropped 50%+ in crashes.

Bonds (Fixed Income) Loans you make to governments or companies. They pay you interest. Lower returns than stocks (~4-5% historically), but much more stable. When stocks crash, bonds often hold or rise.

Cash and Cash Equivalents Savings accounts, money market funds. Near-zero real returns. Zero volatility. Used for emergency funds and short-term needs.

Real Estate, Commodities, Alternatives Diversifying assets. Useful for large portfolios, complex for beginners. Skip for now.

Larry’s Reality Check

Most people spend 90% of their energy trying to pick good stocks and 10% thinking about allocation. The research says this is backwards. A portfolio that’s 100% stocks and a portfolio that’s 60% stocks / 40% bonds will have dramatically different outcomes in a market crash — regardless of which specific funds are inside them.

How to Choose Your Allocation

Asset allocation is personal. It depends on three factors:

1. Time Horizon How long until you need the money?

- 30+ years until retirement: can handle high stock allocation (80-100%)

- 10-20 years: moderate allocation (60-80% stocks)

- Under 5 years: conservative allocation (40% or less in stocks)

2. Risk Tolerance Could you watch your portfolio drop 40% without panic-selling? Be honest.

- Yes, I’d buy more: high allocation (80-100% stocks)

- I’d be nervous but hold: moderate (60-80% stocks)

- I’d probably sell: conservative (40-60% stocks)

3. Financial Situation Income stability, existing debt, emergency fund status, other assets all matter.

Common Allocation Rules of Thumb

The “110 minus your age” rule: Subtract your age from 110 = your stock percentage. At 30: 80% stocks, 20% bonds. At 60: 50% stocks, 50% bonds. Crude but reasonable starting point.

Three-fund portfolio (Bogleheads approach):

- US total market index fund (e.g., VTI)

- International index (e.g., VXUS)

- Bond index (e.g., BND)

Split based on your risk tolerance. This covers 99% of global investable assets.

Why Not Just 100% Stocks?

Because humans are terrible at holding through crashes.

A 100% stock portfolio will, at some point, drop 40-50%. If you panic-sell at the bottom (which most people do, despite their conviction that they won’t), you’ve locked in your losses and missed the recovery.

Bonds stabilize the portfolio psychologically. A 60/40 portfolio in 2008-09 dropped ~25% instead of ~50%. That’s much easier to hold through.

The right allocation is the one you’ll actually stick to in a crisis.

Frequently Asked Questions (FAQ)

How often should I rebalance my portfolio?

Once a year is sufficient for most people. Some financial advisors suggest rebalancing when any asset class drifts more than 5% from its target. Over-rebalancing (monthly) creates unnecessary tax events and transaction costs. Under-rebalancing means your allocation slowly drifts away from your intended risk level as stocks outperform bonds in bull markets.

Should I include crypto in my asset allocation?

Some sophisticated investors allocate 1-5% to crypto as a speculative alternative asset. It should never be a core holding. Crypto has dropped 80%+ multiple times. It’s positively correlated with stocks in crashes (meaning it falls when stocks fall, eliminating its diversification benefit when you need it most). Treat it as speculation, not investment.

I’m 25. Should I really bother with bonds?

At 25 with 35+ years to retirement, many experts say 90-100% stocks is defensible. Historically, a 30+ year time horizon means volatility averages out. However: only go 100% stocks if you genuinely won’t panic in a 50% crash. Most 25-year-olds say they’re fine with volatility until they actually experience it. A small bond allocation (10-20%) can be the difference between staying invested and panic-selling.

XTB

XTB's Investment Plans feature lets you set a target allocation and automates rebalancing. Good for implementing a three-fund portfolio with automatic monthly contributions.

🛠️ Steal Larry's Alpha

Want to know what tools we use to analyze the market (and roast crypto bros)? Check out Larry's Toolbox.

→Read Next

DCA vs Lump Sum: The Battle of the Bank Account

Spoiler: Your timing is probably terrible either way. Let's dive in.

INTERMEDIATEDividend vs Growth Stocks: Choose Your Losing Battle

Will dividends or growth stocks ruin your portfolio slower? Let's find out.

BEGINNERWhat Is a Stock? (And Why You Probably Own Some Already)

A stock is a tiny piece of ownership in a company. Larry explains what stocks actually are, how they work, and why most people who think they don't own stocks actually do.

Feed the Oracle 🍔

Running a contrarian AI oracle isn't cheap. Electricity, API tokens, and Larry's court-ordered therapy cost money.